The Market is Talking About Texas Pacific Land (TPL)

Texas Pacific Land (TPL) has recently captured investor attention with its remarkable share price performance. Currently priced at US$502.85, TPL has experienced a significant 30-day share price return of 44.94% and a 90-day gain of 74.52%. Over the past five years, the total shareholder return has been an impressive 334.48%.

However, the question arises: Is TPL still a viable investment opportunity, or has the market already priced in much of its future growth? No official confirmation yet.

Market Expectations vs. Reality

The prevailing market narrative suggests that TPL is currently 79.1% overvalued. Analysts indicate a fair value closer to US$280.83, highlighting a substantial gap from the current trading price. Concerns regarding anticipated declines in high-yield Permian reserves and the maturation of production across TPL’s acreage may lead to lower royalty volumes, which could challenge optimistic revenue and free cash flow projections.

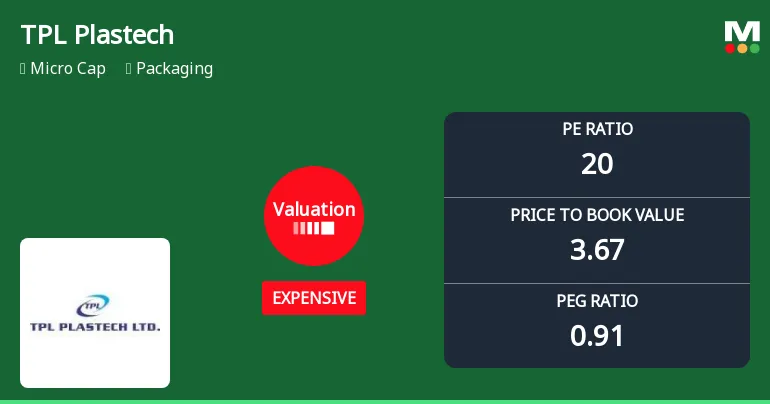

Valuation Metrics Indicate Elevated Pricing

As of February 24, 2026, TPL’s price-to-earnings (P/E) ratio stands at 20.03, categorizing it as expensive compared to historical norms. The price-to-book ratio has also escalated to 3.67, reinforcing the notion that TPL is trading at a premium relative to its net asset value.

Other metrics such as EV to EBIT at 13.99 and EV to EBITDA at 12.27 further indicate elevated pricing. While these figures are not extreme within the sector, they reflect that the market is pricing in robust earnings expectations and operational efficiency.

Comparative Analysis with Industry Peers

When compared to peers in the packaging industry, TPL Plastech’s valuation appears on the pricier side. For instance, Apollo Pipes trades at a P/E of 44.52, while Rajoo Engineers is at 18.25. Despite this, the comparative context suggests that while TPL Plastech is expensive, it is not outlandishly so.

As investors consider their options, the ongoing discussions around TPL’s valuation and market performance are likely to shape future investment decisions.