Introduction

Bank interest rates in Canada play a pivotal role in the financial landscape, impacting everything from personal savings accounts to mortgages. The Bank of Canada (BoC) sets the benchmark interest rate, which influences how much Canadians pay for loans and earn from their savings. With recent fluctuations, understanding these rates is critical for individuals and businesses alike.

Current Trends in Interest Rates

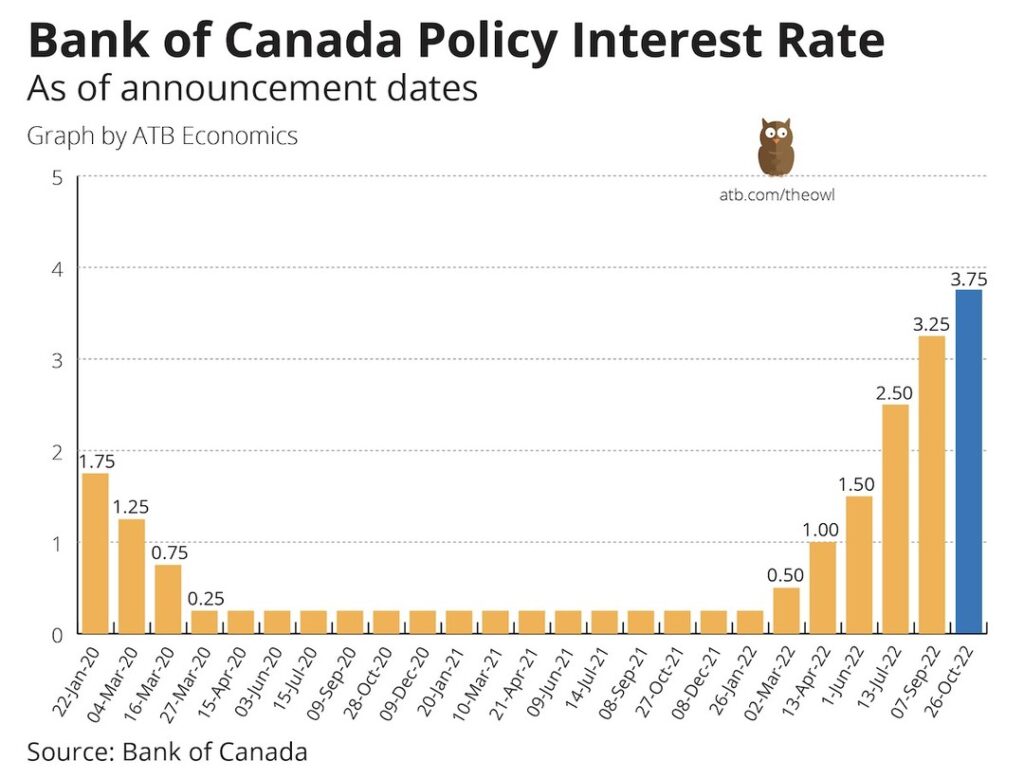

As of October 2023, the Bank of Canada has maintained its interest rate at 5.00%, a level it introduced to combat rising inflation over the past year. This decision has substantially affected both the lending and savings market. Fixed mortgage rates have seen an increase, while variable rates are closely tied to the BoC’s overnight rate, leading to changes in monthly payment amounts for many homeowners.

Impact on Borrowers

The rise in interest rates has significant implications for borrowers. Those with existing variable-rate loans have already begun to feel the pinch of higher monthly payments. The cost of borrowing is climbing, leading many potential homebuyers to reconsider their purchasing plans. According to a recent survey by the Canada Mortgage and Housing Corporation (CMHC), 32% of first-time homebuyers are now delaying their buying decisions due to elevated borrowing costs.

Effects on Savers

Conversely, savers may find a silver lining in these rising rates. High-interest savings accounts and other investment vehicles are starting to offer better returns than in previous years. Financial analysts note that many Canadians are looking to high-interest savings accounts as a viable option to grow their savings. Banks are responding by promoting attractive savings products, with rates reaching as high as 3.5% at various institutions.

Future Outlook

Looking ahead, the future of interest rates in Canada remains uncertain. Economists predict that the Bank of Canada may have to consider additional rate hikes if inflation does not stabilize. Conversely, if inflation decreases and economic growth slows, rate cuts could be on the horizon. As the Bank of Canada navigates these complex economic signals, Canadians must stay informed about how interest rates may affect their financial decisions.

Conclusion

In conclusion, bank interest rates in Canada are a crucial aspect of financial planning for individuals and businesses alike. The current climate of rising rates poses challenges for borrowers while providing opportunities for savers. Staying informed about these changes can help Canadians make better financial choices in an evolving economic landscape.