Introduction

The prime rate in Canada plays a crucial role in the financial landscape, influencing borrowing costs for consumers and businesses alike. It sets the base interest rate that banks charge their most creditworthy clients, thereby impacting a wide range of loans including mortgages, personal loans, and credit cards. Understanding the prime rate is essential for Canadians who wish to navigate their financial decisions effectively, especially amidst changing economic conditions.

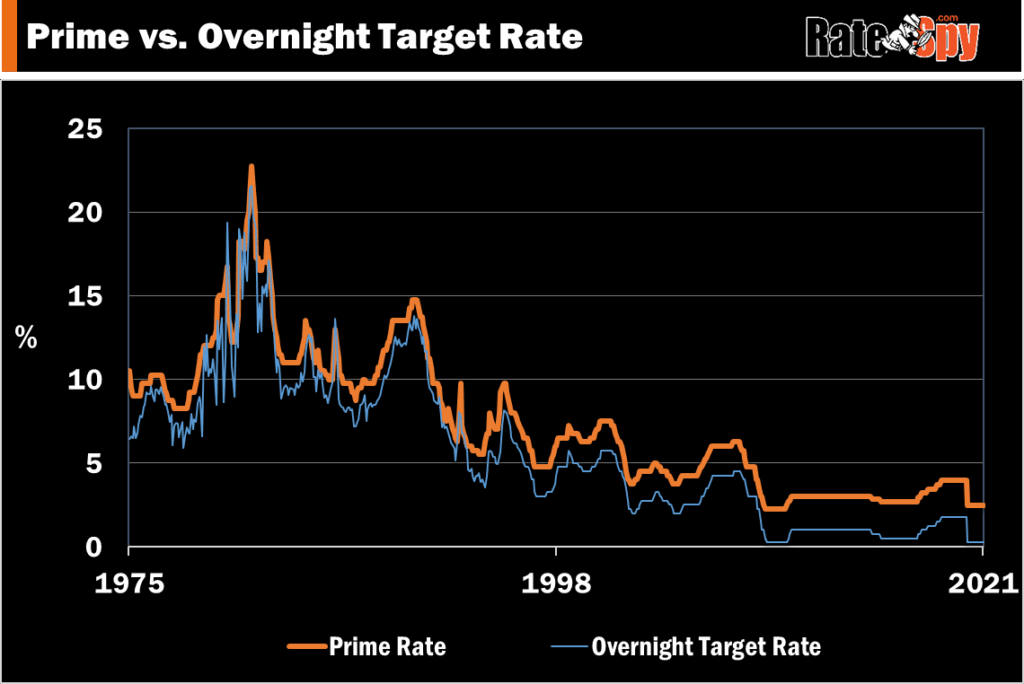

Current Status of the Prime Rate

As of October 2023, the Bank of Canada has maintained a prime rate of 5.45%. This rate has seen increases over the past year, as the Bank seeks to combat rising inflation and stabilize the economy. Since March 2022, the Bank of Canada has increased the rate several times, reflecting its cautious approach to managing economic growth and inflationary pressures.

Impact on Consumers and Businesses

The prime rate greatly affects the cost of borrowing. For instance, an increase in the prime rate can lead to higher interest rates on variable-rate mortgages and loans, affecting monthly payments for homeowners and businesses alike. Financial experts warn that higher borrowing costs may result in decreased consumer spending, which in turn could slow economic growth.

On the other hand, a lower prime rate can stimulate economic activity by making borrowing cheaper. Businesses may take advantage of lower rates to finance expansion or invest in new equipment, while consumers may be encouraged to make larger purchases, such as homes and vehicles.

The Future of the Prime Rate

Looking ahead, analysts predict that the prime rate may be influenced by various factors, including inflation rates, employment figures, and global economic conditions. The Bank of Canada has indicated that it will continue to monitor economic indicators closely to determine future rate adjustments. If inflation stabilizes, there might be room for cuts in the prime rate, offering relief to borrowers.

Conclusion

The prime rate in Canada is not just a financial figure; it is a reflection of the broader economic environment. For Canadians, understanding how the prime rate impacts their personal finances is vital. As we move into 2024, potential rate changes could significantly affect consumer borrowing choices and overall economic health. Staying informed about the prime rate will empower Canadians to make smart financial decisions amid shifting economic landscapes.