Introduction

As Canada continues to evolve demographically, discussions around retirement have grown increasingly important. The aging population and financial trends raise critical questions for individuals preparing for their golden years. Understanding retirement options in Canada is vital for ensuring a secure and comfortable future.

Current Retirement Landscape in Canada

Canada’s retirement system comprises three main pillars: the Canada Pension Plan (CPP), Old Age Security (OAS), and private savings. As of 2023, approximately 40% of Canadians rely primarily on the CPP, with many facing challenges stemming from rising costs of living and inflation. Financial experts recommend that individuals begin saving early to complement these public schemes.

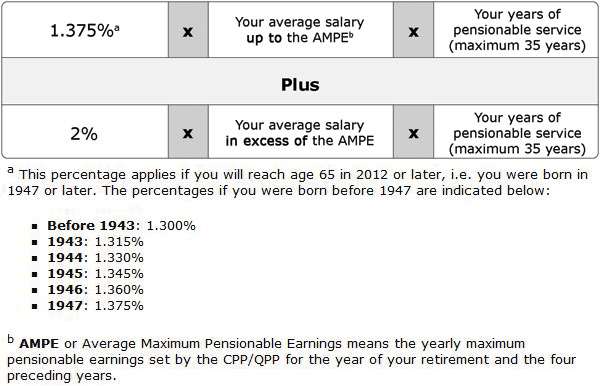

The Canada Pension Plan (CPP)

The CPP is a government-operated program that provides a monthly pension to retired workers based on their earnings during their working life. Recent reforms aim to enhance its sustainability; the contribution rate is gradually increasing from 9.9% to 14.9% over several years. Additionally, early retirement can reduce monthly benefits significantly, making timing a critical decision for many.

Old Age Security (OAS)

The Old Age Security program serves as a universal payment for Canadians aged 65 and older, irrespective of their work history. The OAS payment is indexed to inflation, helping retirees maintain their purchasing power, though eligibility can depend on residency and income levels. Income-tested benefits, such as the Guaranteed Income Supplement (GIS), assist lower-income seniors, but the qualifying thresholds are continually evaluated in light of rising living costs.

Private Retirement Savings

In parallel to public pension plans, private savings play a crucial role in retirement planning. Registered Retirement Savings Plans (RRSPs) and Tax-Free Savings Accounts (TFSAs) are popular vehicles through which Canadians can save for retirement. These accounts allow for tax-deferred growth or tax-free withdrawals, respectively, and are an essential part of a holistic retirement strategy.

Future Trends and Considerations

Looking ahead, several trends are likely to shape the future of retirement in Canada. The rise of the gig economy and remote work has led to non-traditional career paths, which may not contribute sufficiently to pension plans. Moreover, changes in societal norms, including longevity and health, will impact how Canadians view and plan for retirement.

Conclusion

As Canadians face evolving demographic realities, understanding retirement options becomes even more crucial. Comprehensive planning that includes public pensions, private savings, and investment strategies will be key to navigating the future. By taking informed steps today, Canadians can work towards achieving a secure and fulfilling retirement tomorrow.